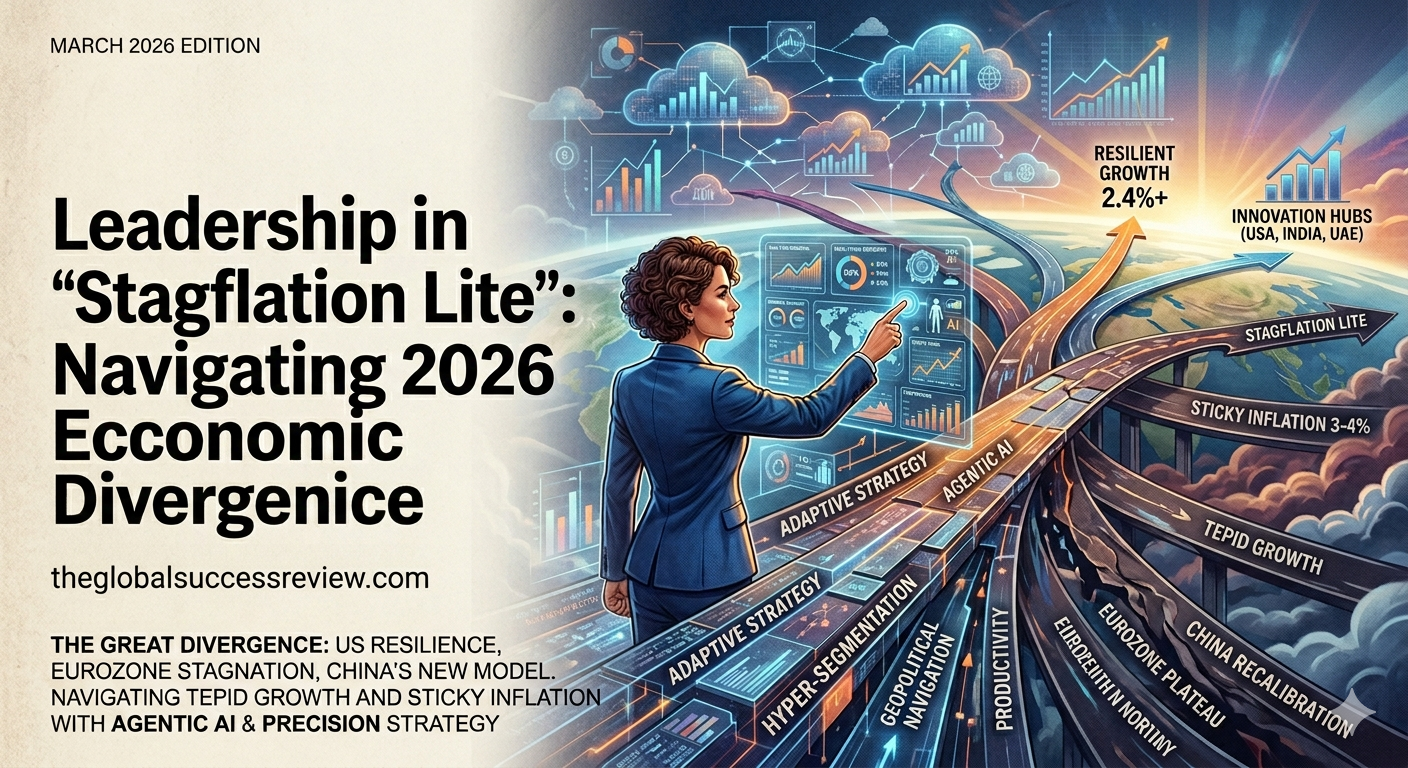

The global economic landscape of 2026 has entered a peculiar phase that economists are calling “Stagflation Lite.” Unlike the crushing double-digit inflation of the 1970s, this era is defined by “sticky” price pressures hovering around 3–4%, coupled with tepid, uneven growth.

For the C-suite, the challenge isn’t a total collapse, but a “Great Divergence” where the U.S. remains resilient, the Eurozone plateaus, and China recalibrates its credit-heavy model. Navigating this requires a shift from defensive posture to adaptive offensive strategy.

1. The Reality of “Sticky” Friction

Inflation has cooled from its 2023 peaks, but the “last mile” of price stability is proving elusive. Wage growth remains robust in services, while 2025’s trade tariffs have permanently baked higher costs into supply chains.

- The Leadership Mandate: Move beyond “across-the-board” price hikes. Leading firms are now using hyper-segmentation AI to identify which customer tiers can absorb cost increases and which require “value-engineered” alternatives to maintain loyalty.

2. Bridging the Productivity Gap with Agentic AI

In a low-growth environment, expanding the workforce is often too expensive. The “Visionary Leaders” of 2026 are using Agentic AI as a macroeconomic shock absorber.

- The Strategy: Instead of simple automation, leaders are deploying autonomous “agents” to manage complex logistics and real-time procurement. This isn’t just about cutting costs; it’s about synthetic scaling, growing output by 5–10% without a linear increase in overhead or energy consumption.

3. Capital Allocation in a “Higher for Longer” World

The era of “free money” is a distant memory. With central bank rates stabilized at a higher floor than the last decade, the cost of capital is a permanent headwind for R&D and expansion.

- The Strategic Shift: We are seeing a move toward “Precision Investment.” Instead of broad market entry, successful CEOs are doubling down on high-margin “niche dominance.” In 2026, being #1 in a $500M sub-sector is more profitable than being #5 in a $5B general market.

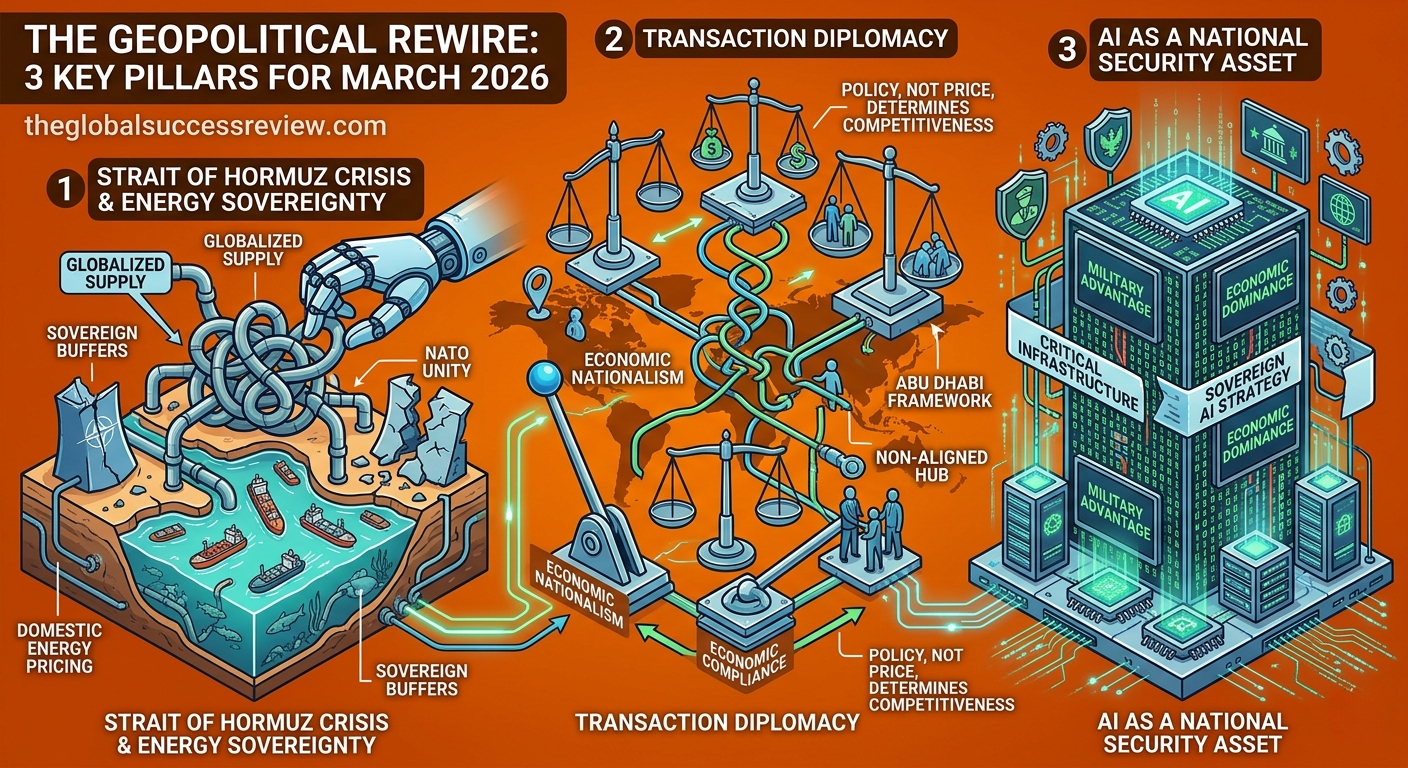

4. Navigating Geopolitical “Trade Corridors”

The “Great Divergence” is fueled by fragmented trade. The U.S.-Canada-Mexico corridor is tightening, while the “principled pragmatism” seen in markets like Abu Dhabi and India is creating new, non-aligned trade hubs.

- The Global Outlook: Supply chain resilience is no longer a “project”, it is the core product. Leaders are diversifying away from single-source dependencies, even if it adds 2% to the COGS (Cost of Goods Sold). They view this 2% as an “insurance premium” against the next geopolitical flare-up.

5. Cultivating “Adaptive Resilience”

In “Stagflation Lite,” the most dangerous thing a leader can have is a rigid 5-year plan. The 2026 winners operate on 180-day rolling forecasts.

“The goal is no longer to predict the future, but to build an organization that can thrive in any version of it.” — The Global Success Review Insight

Conclusion: The 2.4% Growth Secret

While the global average growth stutters, a tier of “Outperformer” companies is consistently hitting 2.4% above-market growth. Their secret? They aren’t waiting for the economy to “return to normal.” They have accepted “Stagflation Lite” as the new baseline and are using technology to decouple their success from the broader macro-stagnation.